Mining can come with negative connotations, but the reality is far more nuanced. On the one hand, production of minerals is highly energy intensive but the rapid proliferation of clean energy technologies (e.g. solar / wind farms, batteries, etc) has driven significant demand for critical minerals that we mine. The industry is in a precarious balancing act, managing the need to increase output whilst reducing emissions and costs.

Here we are diving in to the role critical minerals play throughout the energy transition, the challenges the mining sector faces in supplying those minerals and what we expect for the future of mining.

The Need for Critical Minerals Throughout the Energy Transition

A net zero future will undoubtedly be minerals intensive – virtually all clean energy technologies require critical minerals in some way, shape or form.

Per megawatt (MW) of energy capacity, clean energy technologies are anywhere between 3 to 15 times more mineral intense vs. fossil fuels. When we adjust for typical capacity factors (i.e. per TWh basis), they are over 10 to 20 times more mineral intense. Approximately 3,000 solar panels are needed for 1 MW of capacity of solar PV; this translates to a 200 MW solar PV project that could be as big as 550 American football fields [1].

The carbon footprint in the extraction and processing of critical minerals for renewable energy generation and storage is actually higher than that for fossil fuel generation. But once we take emissions from extracting and burning fossil fuels into account, renewable generation and storage is 6 to 10 times less carbon intensive. This, combined with the often lower LCOE for renewables is driving demand in critical mineral extraction.

The Demand for Critical Minerals Will be Unprecedented

The growth in critical minerals has been strong in recent years with lithium demand rising by 30% in 2023, while nickel, cobalt, graphite and rare earth elements all saw increases in demand ranging from 8% to 15% [4][5].

However, in a net zero 2050 scenario, the growth in critical minerals demand will be a significantly higher. By 2040, demand for key metals is expected to be ~3 – 14 times higher vs. 2023 and clean energy applications will account for more than 50% of most metals demand. At this point, the combined market value of these minerals is forecast to be US$770 billion (vs US$325 billion in 2023) [6].

We Will Face Serious Supply-side Challenges to Meet a Net Zero Future

Across virtually all critical minerals, we expect to face medium to long term supply crunches when considering existing mines and announced projects. By 2030, supply shortfalls of 10% will emerge for copper, lithium and nickel whilst graphite and rare earths will start to see deficits from 2035 onwards [8].

Importantly, geopolitical concentration of supply is highly pronounced across the minerals value chain with the top 3 producing nations in each vertical (notably, China) often controlling the vast majority of mining and refining capacity. This creates dependency on limited sources and a real risk to the deployment of clean energy technologies.

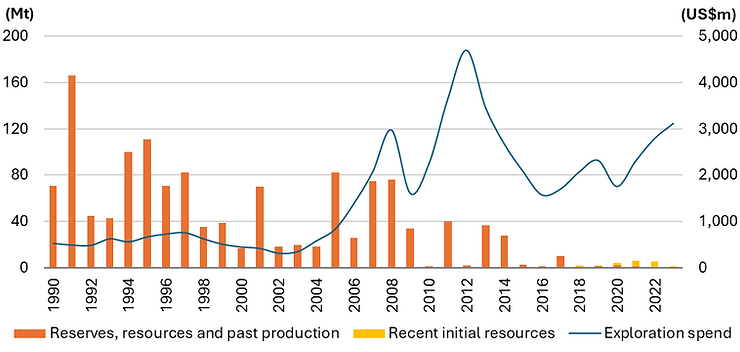

Typically, supply has been replenished through new exploration activity which filters through to resource and reserve definition and ultimately mine development and commissioning. However, taking copper as an example, there have been limited new discoveries in the last five years despite increasing exploration spend. Most of the geologically straightforward copper hosts have been found and extracted with newer discoveries being more complex and lower grade in nature.

For mines in development, the commissioning and build phase has become increasingly challenging due to tougher permitting and increased sensitivity within local communities. For example, Cobre Panama was ordered to close by the Panamanian Supreme Court last year off the back of mass protests whilst Las Bambas in Peru has faced regular road blockages from local communities since the mine opened in 2016.

Project timelines have lengthened significantly – it now takes nearly 18 years to go from discovery to production compared to 13 years for mines that started between 2005 – 2009. Job creation has been weak with the level of new mining engineering graduates continuing to fall whilst many experienced mine workers are expected to retire by 2033 [11].

For the above reasons, the mining majors are choosing to engage in M&A as a means of gaining scale quickly in critical minerals as opposed to building mines organically. For example, BHP has aggressively grown its copper portfolio having acquired OZ Minerals for US$6.4Bn and attempting to merge with Anglo American in 2023 whilst Rio Tinto agreed to acquire Arcadium Lithium for US$6.7Bn in October, 2024.

Minerals Production is Fundamentally Emissions-intensive

Whilst clean energy technologies are set to be the future demand driver, minerals are used in a diversified set of other use cases (whether building roads or constructing buildings) and the industry is highly emissive in general. Estimates suggest that the sector contributes between ~4 – 7% to global greenhouse gas emissions with final energy consumption likely to increase by a factor of ~2 – 8x by 2060 [13][14].

Energy intensity has continued to rise as deposits have matured and grades have fallen to a point where ore mined typically contains less than 1.0% copper (in contrast to 150 years ago where grades were consistently 5 – 10%). Geological / metallurgical complexity has increased over time and traditional methods are requiring increasing amounts of energy to produce the same amount of refined material.

The Role of Technology in Mining

The sector dynamics outlined above are structural in nature and they highlight the need for technology in the sector whether it be to help source new discoveries, improve productivity of existing assets, reduce operational emissions and lower OpEx / CapEx.

However, technology investment in the industry has been relatively low with miners historically spending less than 3% of their EBITDA on R&D vs 8% for materials producers, 30% for industrials companies and 40% for automakers and relevant OEMs [16].

At Twynam, we see promising changes across the industry and renewed interest from investors and strategics in our network to deploy capital into mining technology. We're looking forward to discovering (pardon the pun) the next wave of technologies to decarbonise mining.

References

[2] IEA – The Role of Critical Minerals in Clean Energy Transitions (Page 6)

[3] World Bank Group – Minerals for Climate Action: The Mineral Intensity of the Clean Energy Transition (Page 87)

[4] All demand related figures sourced from IEA – Critical Minerals Outlook 2024

[5] IEA – Critical Minerals Outlook 2024 (Page 6)

[6] IEA – Critical Minerals Outlook 2024 (Page 7)

[7] IEA – The Role of Critical Minerals in Clean Energy Transitions (Page 96)

[8] IEA – Critical Minerals Outlook 2024 (Pages 108, 125, 137, 155, 168 and 178)

[9] IEA – Critical Minerals Outlook 2024 (Pages 108, 125, 137, 155, 168 and 178)

[10] S&P Global Market Intelligence – Major Copper Discoveries (Page 3)

[11] Oregon Group – The Mining Industry if Running Out of Miners

[12] S&P Global Market Intelligence – Major Copper Discoveries (Page 8)

[13] McKinsey – Here’s how the mining industry can respond to climate change

[14] Aramendia, Brockway, Talor and Norman 2023

[15] Brook Hunt / World Copper Ltd

[16] White & Case – Technology – The hottest commodity in the mining & metals sector